Tailoring a Swift Change to Deposit Insurance

Following the collapse of Silicon Valley Bank, Signature Bank, and the sale of First Republic, there’s been an increasing interest by regulators to reform the US deposit insurance scheme to fully protect the banking system from future bank runs.

The Perfect Storm for Bank Runs

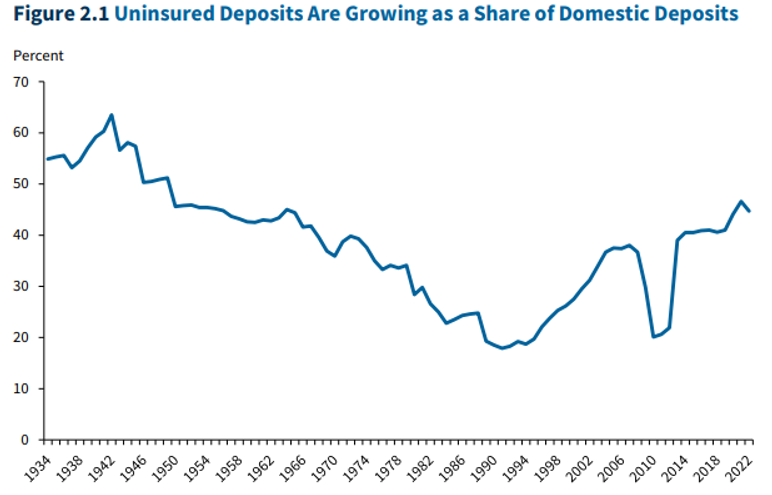

Panic among deposit holders lit the initial spark that led to the failures of Silicon Valley Bank and Signature Bank with advances in technology hastening the pace at which these bank runs could occur. With Federal Deposit Insurance Corporation (FDIC) insurance coverage at only $250,000 per depository institution and uninsured deposits comprising approximately 43% of domestic bank deposits, it’s no wonder that deposit flight occurred at the shakiest of banks. The crisis was in part mitigated by the Federal Reserve’s Bank Term Funding Program (BTFP), which effectively allowed banks to improve liquidity by borrowing against the par value of their assets. Longer-term, however, regulators may focus on changes to the FDIC deposit insurance scheme to improve financial stability.

Source: FDIC

The US Deposit Insurance Scheme

Established in 1934, the Federal Deposit Insurance Corporation (FDIC) provides insurance on deposits up to $250,000 through its deposit insurance fund. This is funded through bank assessment fees that currently range from 3 – 42 bps based on a bank’s total liabilities. The resolution of the three banks listed above has cost the fund an estimated $32 billion.[1] Perhaps, if deposit insurance limits were higher, the March regional banking crisis could have been mitigated. In May 2023, the FDIC published the report “Options for Deposit Insurance Reform” which attempts to tackle changes to the deposit insurance scheme and proposed three options that it hopes will stem the tide of future bank runs: Limited Coverage, Unlimited Coverage and Targeted Coverage.

Limited Coverage

Under FDIC’s proposal, Limited Coverage will maintain the current deposit insurance structure of covering all deposit type accounts on a combined basis with an increased insurance amount above the current $250,000 threshold. Despite higher insurance levels, the FDIC acknowledges that this scheme by itself will not solve the run risk associated with a high concentration of uninsured deposits because any immediate deposit outflows could still destabilize the banking system. They foresee, including other regulatory actions such as limiting bank reliance on uninsured deposits, reducing the incentive for depositors to run or even limiting the ability for depositors to withdraw funds as necessary to prevent future bank runs under the Limited Coverage proposal.

Unlimited Coverage

Unlimited Coverage would provide full insurance for all deposits and ultimately remove the run risk entirely. While this would be most effective at preventing future bank runs, implementing this scheme may increase bank risk-taking with deposits being effectively fixed to the balance sheet. This could also severely increase the assessment fees to fund the deposit insurance fund. Full deposit insurance could also disrupt other parts of the financial markets as a full protection of deposits would discourage depositors from putting cash elsewhere, leading to less liquidity in the short-term cash investment space and making it more expensive for businesses to borrow.

Targeted Coverage

Targeted Coverage would allow different levels of deposit insurance for different types of accounts, with the aim of providing higher coverage or even unlimited coverage for business payment accounts. Although payment accounts are not clearly defined, the FDIC intends to target higher insurance levels for deposit accounts that do not pay interest and primarily are used for payroll and expenses. Comparatively, deposit insurance for regular interest-bearing deposit accounts could stay at the current levels. The FDIC expects this scheme would have large financial stability benefits and fewer moral hazard concerns compared to other proposals but faces challenges in delineating between business payment deposits and other deposits. There is also concern for limiting the ability of depositors to seek higher insurance amounts by circumventing the intended regulation.

Additional Supportive Options

The report proposed additional supportive options to be implemented with either Limited Coverage or Targeted Coverage. Secured Deposits for Large Uninsured Deposits would match deposits (viewed as short-term liabilities on bank balance sheets) with securitized short-term assets that would effectively function as additional capital support for uninsured deposits. The FDIC believes this measure will reduce the burden of monitoring bank balance sheets and instead focus efforts on monitoring collateral. Additionally, the FDIC proposed Limiting Convertibility of Deposits Above the Deposit Insurance Limit which would place constraints on the ability of large depositors to withdraw funds with the restrictions being either set by the banks or triggered by financial stress. Constraints could include restricting withdrawals to a percentage of the account balance within a certain period of time; thus, incentivizing large depositors to seek alternatives. Additionally, this could severely slow down a bank run to allow the FDIC time to resolve the situation.

Conclusion

The ultimate goal of deposit insurance coverage is to make deposits stickier at financial institutions and cut off an age-old vulnerability to all banks by preventing bank runs. Because the FDIC does not have unilateral authority to raise the insurance limit, any changes would require an act of Congress. We expect deposit insurance coverage to increase once Congress gets through the current debt ceiling deliberations. No matter which form or structure deposit insurance takes, we expect depositors will rely more heavily on cash investments through separately managed accounts and commingled money market funds as they become more aware of the yield disadvantage bank deposit accounts may have relative to their risk profile. The higher fees that would be imposed on the banks would ultimately flow through to the customer via lower yielding bank products. More than ever, a prudent manager should seek to allocate a safe liquid bucket that is fully insured through FDIC coverage and search for acceptable yield through cash investments. To read more on our view of uninsured deposits, read our whitepaper – An Expensive Lesson on Uninsured Deposit Risk in Cash Management.

1Remarks by Chairman Martin J. Gruenberg on “Oversight of Financial Regulators: Financial Stability, Supervision, and Consumer Protection in the Wake of Recent Bank Failures” before the Committee on Banking, Housing, and Urban Affairs, United States Senate – https://www.fdic.gov/news/speeches/2023/spmay1723.html#:~:text=The%20remaining%20estimated%20loss%20from,will%20directly%20impact%20the%20DIF.

Please click here for disclosure information: Our research is for personal, non-commercial use only. You may not copy, distribute or modify content contained on this Website without prior written authorization from Capital Advisors Group. By viewing this Website and/or downloading its content, you agree to the Terms of Use & Privacy Policy.