Integrated Oil & Gas Majors Position for Peak Demand

While most major integrated oil and gas companies have expressed alignment with the Paris Agreement, efforts made by U.S. players to address climate change with a transition to more renewable energy sources have fallen short in comparison to their European counterparts. As some drag their feet on sustainability efforts, governments, world organizations and financial institutions continue to pressure companies to align with climate-focused goals. Those that fail to take action to align themselves with the Paris Agreement will likely face social and regulatory pressure which, along with a weakening revenue outlook, might result in weaker business and financial profiles.

For institutional cash investors, the transition to renewables by oil and gas majors will require new levels of portfolio oversight. Anticipating the possibility of credit downgrades may require asset managers to reposition their short-, medium-, and long-term holdings of specific oil and gas credits, as each of the majors proceeds with the transition according to its own strategy and on its own schedule. Risk reduction will require increased attention to environmental, social, and governance (ESG) investing guidelines.

A Peak Followed by a Long Plateau

Many energy-related organizations now expect oil demand to peak or plateau before 2040, with BP declaring in September 2020 that the market may never recover to pre-pandemic levels of 100 million barrels per day, albeit this is conservative by many estimates. Even OPEC has identified a plateauing of oil demand after 2035. Specifically, they expect global demand will hit 107.9mn b/d in 2035, 17.3mn b/d above its 2020 level, after which demand will plateau in the long run.

Similarly, the International Energy Agency (IEA) has forecasted that global oil demand growth will come to an end in the next decade. This peak will be followed by a slow decline, as in the absence of a large shift in government policies, a rapid decline in global oil demand is unlikely, according to the IEA. Major oil and gas companies generally align with these assessments. Exxon, for example, forecasts a 20% increase in demand from 2017 to 2040 due to a growing global population and increasing prosperity, after which it expects to see a plateau and eventual decline.

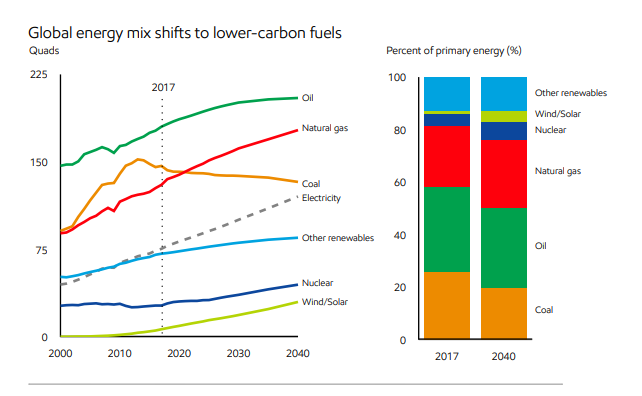

As can be seen in the figure below, while the increase in demand for fossil fuels will be supported by continued reliance on natural gas, demand for oil will likely taper.

Source: ExxonMobil

Shell expects peak oil demand will occur even earlier, in 10-15 years. Similar to Exxon, they view that continued dependence on oil and gas will be driven by a growing world population and increasing prosperity. Despite the similarity in assumptions, Exxon and Shell have taken contrasting levels of action related to the transition to a low carbon economy.

European Majors are Moving Faster Than U.S. Players

Generally, the European majors are further along than U.S. players, with bolder and more aggressive action toward sustainable business models, driven in part by a greater push from regulators to curb major emissions. Like many European peers, Shell has committed to net-zero emissions by 2050 or sooner by setting short-term, incremental goals and tracking its net carbon intensity in the years before. Shell plans to transition its capital allocation toward low carbon energy sources, including hydrogen and biofuels, while shifting investment away from traditional oil and gas businesses. Additionally, its net carbon footprint-related targets are linked to executive compensation, with sustainable development accounting for 20% of the 2020 Executive Scorecard which helps determine annual bonuses.

Shell has also committed to increasing investment in its New Energies segment, which covers its renewables business, to 10% of its capital budget. Despite industry leading initiatives, The Hague District Court, which governs the region in which Shell’s headquarters reside, ordered Shell to reduce its scope 3 carbon emissions by 45% of 2019 levels by 2030. Heightened regulatory scrutiny, coupled with cultural differences has created vast discrepancies between the carbon initiatives of U.S. and European majors.

S&P compared the energy majors’ transition strategies in December 2020, documenting the rankings in the below infographic. As shown, European majors are consistently ranked higher compared to U.S. majors in terms of total installed renewable capacity and carbon capture utilization and storage (CCUS), as well as their efforts across downstream retail, sustainable transport and battery storage.

![]()

Source: S&P Global

As evidenced by the infographic above, up until very recently, Exxon’s sustainability-related initiatives had been next to nothing. In response to pressure from activist investors, Exxon announced with its fourth quarter 2020 earnings the creation of its new Low Carbon Solutions business segment. The segment will continue to develop and commercialize Exxon’s carbon capture and storage capabilities. Despite this move, activist investment firm Engine No. 1 has been pushing the company to adapt its business model to a low carbon economy since December and won three seats on Exxon’s board at the company’s annual shareholder meeting this year. The election of Engine No. 1’s nominees sends a clear message that investors desire oil majors to take immediate, bold steps to adapt to a transitioning economy.

Industry Majors Face Increasing Pressure to Act

As mentioned in Capital Advisors Group’s most recent yearly outlook, over the past two years there has been significant action taken on the ESG front. This includes BlackRock’s Larry Fink calling on all companies in his 2021 letter to CEOs to “disclose a plan for how their business model will be compatible with a net zero economy.” And Bank of America joined firms including JP Morgan, Citi, Goldman Sachs, Morgan Stanley, and Wells Fargo in committing not to finance oil and gas exploration in the Artic in response to activist pressure.

Additionally, both the E.U. and the U.S. have taken steps to account for the risks that a transition to a carbon neutral economy pose. This includes the EU instituting the Sustainable Finance Disclosure Regulation, which will hasten the integration of sustainability considerations into the financial system, as well as President Biden signing an executive order on climate-related financial risks which aims to incorporate environmental considerations and risks into the financial system. Both acts will help develop sustainability considerations into impactful and consequential investment tools.

Cash Portfolios Need to Factor Sustainability into Risk Profiles

If companies do not take significant action to align with a net-zero emissions economy, consequences could include decreased investment confidence, weakened business profiles and eventual rating downgrades. One such example was S&P’s downwardly revised oil and gas industry risk assessment at the beginning of the year, from intermediate risk to moderately high risk, putting negative pressure on most integrated oil and gas names. Among the considerations resulting in the downgrade were significant challenges and uncertainty associated with the energy transition.

Given the recognized risks associated with the transition towards a more renewable future, institutional cash investment portfolio managers will need to carefully assess how it will affect oil and gas companies’ credit worthiness. Until recently, such assessments were highly subjective, requiring comparison of much “apples and oranges” data. However, there is a growing body of guidance for the new discipline of ESG investing designed to provide analysts with common measures of progress toward sustainability goals. CFOs and corporate treasury groups that come up the learning curve quickly will be able to reduce risk in their cash portfolios and be positioned to make safer and more productive investments in a sustainable future.

For more on the ins and outs of ESG investment oversight by institutional cash investors, see our additional content on ESG performance and measurement guidelines:

Please click here for disclosure information: Our research is for personal, non-commercial use only. You may not copy, distribute or modify content contained on this Website without prior written authorization from Capital Advisors Group. By viewing this Website and/or downloading its content, you agree to the Terms of Use & Privacy Policy.